Third European Hydrogen Bank auction: what €0.44/kg tells Latvian hydrogen developers about the next call

The third European Hydrogen Bank auction awarded €1.09 billion to nine projects at bid prices as low as €0.44/kg — and Latvia was not on the winners' list. Here is what the IF25 result tells Latvian hydrogen developers about how to position the next bid.

NEWS

HydrogenLatvia

5/9/20266 min read

Brussels announced the IF25 results on 7 May. Nine winners, €1.09 billion awarded, and a competition that was more than seven times oversubscribed. The harder reading is between the lines — and that reading matters now for everyone working on a Baltic hydrogen project.

A market-clearing auction with very real lessons

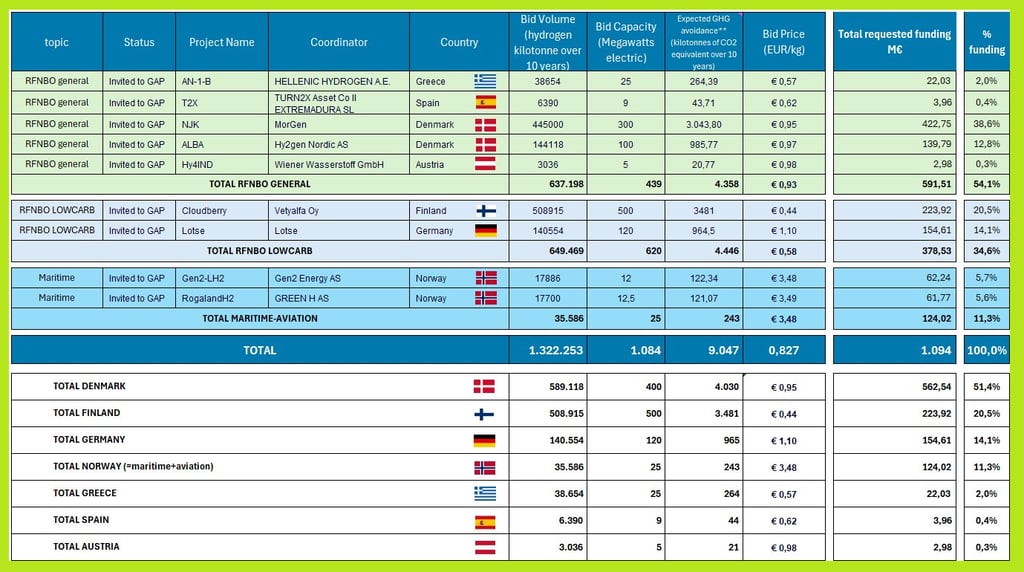

On 7 May 2026 the European Commission published the results of the third auction held under the European Hydrogen Bank — the IF25 round of the Innovation Fund. Nine projects were selected across seven countries in the European Economic Area, sharing €1.09 billion in EU funding sourced from the EU ETS. Together they will deploy almost 1.1 GW of electrolyser capacity and produce 1.3 million tonnes of RFNBO and low-carbon electrolytic hydrogen over their first ten years of operation, avoiding an estimated 9 million tonnes of CO₂-equivalent emissions.

Two numbers are worth pausing on. The first basket — for renewable RFNBO hydrogen production — drew 50 bids requesting €7.3 billion against a €600 million pot. That is more than seven times oversubscribed, with serious developers competing on price. The second number is the lowest winning bid: €0.44 per kilogram, secured by Tuulialfa's Vetyalfa subsidiary for its 500 MW Cloudberry project in Vaaka, Finland. The highest winning bid in the maritime/aviation basket reached €3.49/kg — and that basket was actually undersubscribed.

Across the three baskets the price spread tells the whole story: bidders chasing the largest pots are willing to accept very thin subsidies; bidders going after the niche topic are not. The market is no longer guessing what RFNBO hydrogen needs to clear at the EU level. It is showing us.

How the three baskets actually performed

Basket one — RFNBO hydrogen production — closed with five winners across Greece, Spain, Denmark (two projects) and Austria, taking €592 million between them, with bids from €0.57/kg to €0.98/kg. Hellenic Hydrogen, a Motor Oil Hellas and Public Power Corporation joint venture, took the lowest winning slot at €0.57/kg for the first 25 MW phase of a 100 MW Greek plant. Greece and Austria are first-time appearances on the winners' list.

Basket two opened up to both RFNBO and low-carbon electrolytic projects. Five bids worth €800 million chased a €400 million pot. Two winners emerged — one in Finland, one in Germany — for a combined €379 million. The Finnish Cloudberry project took €0.44/kg; Copenhagen Infrastructure Partners' 120 MW Lotse e-fuel project in Germany took €1.10/kg.

Basket three was the new one, designed for projects supplying maritime and aviation offtakers. It received only three bids and was undersubscribed by €137 million. Both winners are Norwegian — Gen2 Energy at €3.48/kg and GreenH at €3.49/kg — and both are small projects, around 12 MW each. The pricing here reflects exactly what shipping and aviation are willing to pay for certified molecules right now: a premium that is currently still seven to eight times higher than the cheapest grid-connected production.

Beyond the EU pot, Spain and Germany are running national tracks through the Auction-as-a-Service mechanism. Germany has lined up €1.3 billion for RFNBO projects feeding into the planned Danish-German hydrogen pipeline; Spain has earmarked €304 million for national RFNBO and a further €136 million for maritime and aviation offtake. Three Spanish projects and three Danish ones from the IF25 reserve list are already in line for AaaS grant agreements.

The signal for Latvian hydrogen ecosystem stakeholders

Latvia did not appear on the IF25 winners' list. That is not a surprise — there is no operating Latvian electrolyser project at FID stage today — but the result is still the most useful market data the sector has had in twelve months. Latvian hydrogen ecosystem stakeholders preparing for the fourth auction (or for national tracks via Auction-as-a-Service) need to read this round as a value-engineering brief, not just as news.

Five things the IF25 result tells us, in order of how directly they should change a Latvian bid:

The price ceiling for serious RFNBO bids is now under €1/kg in basket one. A Baltic project pricing above that line will need a very specific reason — maritime/aviation offtake, or an Auction-as-a-Service track — to be competitive at all. Pricing discipline starts on day one of the project economics, not at submission.

Winning bids increasingly come from countries that have transposed RED III transport targets into national law. Finland's Cloudberry win and the German basket-two slot both sit on top of national demand pulled forward by transport quotas. Latvia's transposition status of RED III — and how visibly the country signals it to bidders — is now part of the project economics, not just regulatory housekeeping.

The interconnector matters. The reason Danish projects keep winning at competitive prices is the planned Danish–German hydrogen pipeline plus Germany's €1.3 billion AaaS pot for projects feeding it. The Nordic-Baltic Hydrogen Corridor — a Project of Common Interest with €6.8 million of CEF feasibility funding deployed — is the equivalent narrative for Latvian, Estonian and Lithuanian projects. It is also a credibility multiplier in front of EU evaluators and offtakers, and it is currently underused in Latvian project pitches.

Maritime and aviation offtake is a structurally different market with structurally different prices. Basket three was undersubscribed at €3.48–3.49/kg, which says two things at once: there is room for credible bidders, and the certified-offtake side is still thin. CIS Liepaja's MoU with NorSAF for eSAF feedstock, Riga's Freeport recent e-methanol initiative and Riga Airport's BSR HyAirport involvement involvement, put Latvian projects unusually well-placed to bid into this topic if the offtake architecture is wired tightly enough to qualify.

Scale is doing more work than chemistry. The €0.44/kg Cloudberry project is 500 MW. The cheapest basket-one winner runs 25 MW in its first phase, but it is the first phase of a 100 MW asset. The auctions reward projects that can credibly absorb the subsidy at industrial scale and demonstrate it. CIS Liepaja's stated build-out toward roughly 21,200 tonnes of green hydrogen per year by 2030 — backed by Vindr's 150 MW of dedicated wind PPA — is the only Latvian project today that maps cleanly onto the scale profile that wins.

What should change in Latvian bids before the next call opens

The IF25 result is a free post-mortem for projects that will bid into the fourth round. A few practical adjustments will land more reliably than another pass at narrative polish:

Build the bid around a verified offtake stack, not a production curve. The lowest-priced winners are the ones who can demonstrate that their molecules are spoken for — through transport-sector demand, through pipeline access to a regulated quota market, or through aviation/maritime contracts. Latvian developers have credible offtake stories available (NorSAF for eSAF, German RED III demand via the Nordic-Baltic Corridor, Riga Airport for BSR HyAirport). The work is to translate those into letters of intent, term sheets, and capacity commitments that survive the eligibility filter.

Stress-test the bid price against €0.57–€1.10/kg. If a Latvian project economics model only works at €1.50/kg or above, the question to answer before submission is what changes — wind PPA structure, electrolyser CAPEX assumption, financing stack — that brings it below €1/kg. The previous two auctions ended at higher clearing prices; this one effectively re-set the bar.

Decide deliberately between the EU track and Auction-as-a-Service. Spain and Germany have just shown that AaaS can route national money into projects that did not clear the EU pot but ranked in the reserve list. Latvia is not currently running an AaaS process, but the format is open to all Member States. For developers, that opens a strategic question: is the bid pitched at a profile that fits a future Latvian or Lithuanian AaaS track, or only at the EU pot? Both answers are valid; the cost of not deciding is high.

Use the Nordic-Baltic Hydrogen Corridor as a structural credibility argument, not a footnote. Connection to a PCI-status corridor with deployed CEF feasibility funding is exactly the kind of infrastructural narrative IF25 winners benefited from. Latvian bids that lead with port plus corridor plus offtake — rather than production capacity in isolation — should rank visibly higher on the qualitative side of the evaluation.

The bigger picture for the Latvian hydrogen ecosystem

There is a temptation to read "no Latvian winner" as a verdict. The more accurate reading is that the IF25 round set the price at which European RFNBO is now expected to clear, and Latvian projects are early enough in their development cycle that the next twelve months are when bid-readiness is actually built. CIS Liepaja in Liepāja SEZ, the NorSAF eSAF facility, Vindr's 900 MW Latvian renewables pipeline, BalticSeaH2's cross-border valley work and Riga Airport's BSR HyAirport role together describe a project portfolio that is closer to being IF26-ready than the auction headlines suggest.

The fourth auction has not been confirmed in detail yet, but Hydrogen Europe is publicly advocating for the European Hydrogen Bank to continue, accompanied by full implementation of RED III and rapid infrastructure deployment. That is the window. Latvian hydrogen ecosystem stakeholders who use the next two quarters to harden offtake contracts, lock down PPA structures, and write bids against the €0.44–€1.10/kg reality of basket one will be in a different category of preparedness when the call opens.

Grant agreements for the IF25 winners are expected to be signed by Q4 2026, with financial close required within 30 months and entry into operation within 60 months of signature. That timeline is the same one Latvian developers are working against. The auction did not close a door; it published the threshold.

Source: EU awards over €1 billion to European hydrogen projects to accelerate the clean transition